The wealth individuals build over a lifetime often represents far more than financial value. It reflects years of discipline and sacrifice aimed at securing a comfortable retirement and providing for loved ones. Yet one of the most important questions in financial planning is not simply how to grow or spend wealth, but how to transfer it thoughtfully and efficiently. Doing so requires a comprehensive estate planning approach that integrates tax considerations, personal goals, and the broader concept of legacy.

Despite its importance, a 2025 survey found that fewer than one in three Americans report having a will, and more than half say they have no estate plan at all. Without a proper structure in place, wealth that took decades to build can be eroded by taxes, legal complications, and unintended distributions. Advanced estate planning addresses this by creating a coordinated approach to maximize the efficient transfer of assets to the people and causes that matter most.

Establishing the Right Framework for Wealth Transfers

Every estate plan is shaped by three foundational questions: what assets are being transferred, to whom, and when. The type of assets involved influences which strategies are most appropriate. Cash and publicly traded securities are generally the most straightforward to transfer, while real estate, closely held business interests, and alternative investments introduce complexity due to valuation challenges and divisibility issues.

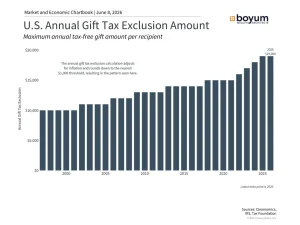

Identifying beneficiaries early is equally important. Whether assets are destined for a spouse, children, grandchildren, or charitable organizations, each beneficiary type may call for different planning strategies. The timing of transfers also plays a key role. By making completed gifts during one’s lifetime, a donor can take advantage of annual gift exclusions to increase the amount of tax-free transfers. In 2026, the annual gift exclusion is $19,000 per recipient, or $38,000 for married couples electing to split gifts. Executed consistently over time, this approach can remove a meaningful portion of taxable estate value.

Several strategies can be mapped to specific estate planning goals. For those seeking to minimize estate taxes and transfer future appreciation to the next generation, irrevocable trusts offer a useful solution. A common example is a Grantor Retained Annuity Trust (GRAT), where the grantor transfers assets into a trust and receives annuity payments over a set term. If the grantor survives the trust term, the remaining assets pass to beneficiaries outside of the taxable estate.

For families with philanthropic goals, a Charitable Remainder Trust (CRT) allows the grantor to designate beneficiaries to receive income for a set term, with the remainder passing to a designated charity. This approach provides both gift tax and income tax deductions for the charitable remainder interest. CRTs work especially well with highly appreciated assets such as real estate or concentrated stock, converting a low-yield, high-gain asset into a tax-advantaged income stream while supporting philanthropic objectives.

Families with business interests or illiquid assets require additional planning around liquidity and continuity. Buy-sell agreements specify how ownership transfers if an owner passes away or becomes incapacitated, while key-person life insurance can provide liquidity without requiring a forced sale. Family Limited Partnerships (FLPs) allow senior family members to transfer ownership interests to the next generation while retaining control as the general partner. Because limited partnership interests lack control and marketability, they may be eligible for valuation discounts, enabling families to transfer more value within gift and estate tax exemption limits.

Estate Planning Is an Ongoing, Lifelong Process

Estate planning is not a one-time exercise. It requires ongoing monitoring and adjustments as personal circumstances and fiscal policies evolve. As families grow across generations, the complexity of wealth transfers increases. The Generation-Skipping Transfer Tax (GSTT) is particularly relevant, as it applies to transfers made to recipients two or more generations younger than the donor. With careful planning, donors can reduce or avoid this additional transfer tax through various strategies.

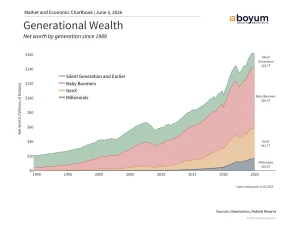

Policy changes can also reshape outcomes over time. Federal estate and gift tax exemptions have shifted significantly over the years, from as low as $675,000 in 2001 to as high as $15 million per individual today. The 2017 Tax Cuts and Jobs Act doubled the exemption amount, and subsequent legislation made these higher thresholds permanent. State-level rules add further complexity, as some states impose their own estate or inheritance taxes with exemption thresholds that differ from federal rules.

For example, Minnesota currently imposes its own estate tax with a $3 million exemption per individual, meaning estates above that level may be subject to state estate tax even if no federal estate tax is owed. As a result, residency and domicile decisions can carry significant financial implications for some families.

All of these strategies work best when integrated with one another and aligned with broader lifetime gifting, succession, and philanthropic goals. Starting early and continuously refining a plan to reflect changing circumstances and objectives is key to long-term success.

At Boyum Wealth Architects, our team helps clients execute a coordinated approach designed to preserve wealth, reduce taxes, and ensure assets are transferred to the right people in the most effective way and at the appropriate time. Please feel free to reach out to any member of our team with questions.

References

1. https://www.caring.com/resources/wills-survey

2. https://www.irs.gov/businesses/small-businesses-self-employed/whats-new-estate-and-gift-tax

3. https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendmentsfrom-

the-one-big-beautiful-bill

Copyright © 2026 Clearnomics, Inc. All rights reserved.

The information contained herein has been obtained from sources believed to be reliable; however, it may not be complete, and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made regarding the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and other information provided are subject to change without notice. All reports posted on or through [www.clearnomics.com](http://www.clearnomics.com), or any affiliated websites, applications, or services, are issued without regard to the specific investment objectives, financial situation, or particular needs of any recipient and should not be construed as a solicitation or offer to buy or sell any securities or related financial instruments. Past performance is not necessarily indicative of future results. Company fundamentals and earnings may be referenced periodically but should not be construed as a recommendation to buy, sell, or hold any company’s stock. Likewise, any predictions, forecasts, or estimates regarding financial markets should not be interpreted as recommendations to buy, sell, or hold any security, including mutual funds, futures contracts, exchange-traded funds, or similar investment vehicles. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. Any unauthorized reproduction, distribution, or other use of material from Clearnomics, Inc. may constitute willful infringement of copyright and other proprietary and intellectual property rights, including rights of privacy. Clearnomics, Inc. expressly reserves all rights relating to its intellectual property, including, without limitation, the right to restrict the transfer of its products and services and to monitor usage through electronic tracking technology and any other lawful means now known or later developed. Clearnomics, Inc. reserves the right, without further notice, to pursue all available civil and criminal remedies to the fullest extent permitted by law for any violation of its rights.